H.R. 7024, the Tax Relief for American Families and Workers Act of 2024, was passed by the House last week and is now moving to the Senate for consideration. The bill would change the Child Tax Credit (CTC) in several ways. The two most contentious changes are a one-year lookback for the refundable portion of the CTC—which would allow parents to use their earnings in the previous year to calculate their CTC if it produces a higher benefit—and applying the refundable CTC on a per child basis. Whereas under existing law the refundable CTC phases in at a 15 percent rate for all families, under H.R. 7024 it would phase in at a rate of 15 percent times the number of children (e.g., a 45 percent rate for a family with three children).

In a previous post, we showed how the per-child benefit provision would weaken the incentive for single parents to move from part-time work to full-time work. For example, we calculated that the effective tax on moving into full-time work would rise by 14 percentage points for a single parent with three children who earns $20 per hour. We concluded that, by discouraging greater earnings, H.R. 7024 could weaken upward mobility.

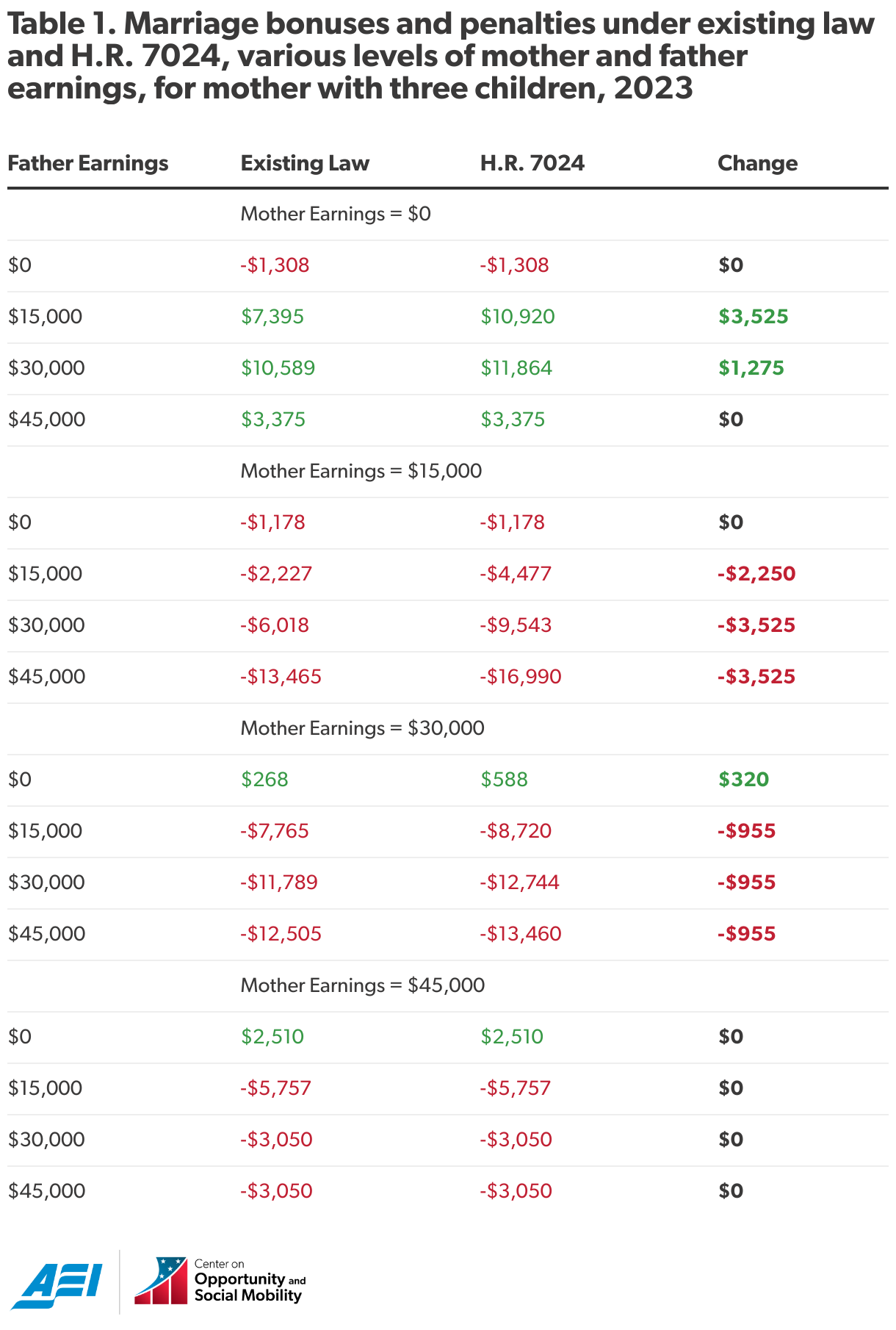

This post describes another way in which H.R. 7024 could weaken upward mobility—by increasing the marriage penalty for parents with multiple children. The marriage penalty refers to the increased taxes and reduced transfers a mother and father experience as a result of getting married, relative to a scenario in which each parent files taxes and claims transfers separately. It is also possible to experience a marriage bonus, in which taxes fall or transfers rise as a result of marriage. Policymakers have expressed growing concern over marriage penalties, in light of declining marriage rates and the growing prevalence of single parent families. Table 1 below calculates the marriage penalty (in red) or marriage bonus (in green) for a mother with three children. The penalties/bonuses account for changes in federal income tax (including the Earned Income Tax Credit and CTC), payroll taxes, and Supplemental Nutrition Assistance Program (SNAP) benefits when marrying the father. The father is assumed to have no other children except for those he shares with the mother. When unmarried, the mother and father are assumed to live separately for purposes of qualifying for SNAP. We show the penalty/bonus under existing law and under H.R. 7024. The final column indicates how the penalty/bonus would increase or decrease due to H.R. 7024. Negative values (in red) mean that the proposed law would make marriage penalties worse.

Note: Father is assumed to have no children except for those he shares with the mother. First column indicates father’s earnings. Second column (existing law) and third column (H.R. 7024) show the change in post-tax, post-transfer income (accounting for federal income tax, federal payroll tax, and Supplemental Nutrition Assistance Program benefits) received by a mother of three children and father in aggregate, due to marriage. A positive change indicates a marriage bonus (in green) and a negative change indicates a marriage penalty (in red). Fourth column indicates the change in the marriage bonus or marriage penalty. For existing law, we apply 2023 tax law without the H.R. 7024 changes, except that we apply the proposed $1,800 maximum refundable CTC. The per-child refundable CTC is 45 percent of earned income above $2,500 before phasing out as the non-refundable CTC phases in. We apply SNAP benefit parameters that took effect starting October 1, 2023, and we assume shelter costs of $1,146 per month for a single parent without children (median gross rent for 1 bedroom unit in 2022) and $1,449 for a single parent or married couple with three children (median gross rent for 3 bedroom unit in 2022), and no other deductions. We assume the mother and father apply for SNAP separately when not married.

From the top panel, we see that under existing law mothers with no earnings receive a marriage bonus from marrying a working father with modest earnings. H.R. 7024 would increase these marriage bonuses, by as much as $3,500 when marrying a father with $15,000 of annual earnings.

From the second panel, we see that under existing law mothers with annual earnings of $15,000 face marriage penalties. H.R. 7024 would worsen these marriage penalties. For example, the penalty for marrying a father with $30,000 or $45,000 would grow by $3,500.

From the third and fourth panels, we see that mothers with earnings of $30,000 would see their marriage penalties grow by about $950 when marrying working fathers, and that mothers with earnings of $45,000 would see no change in their marriage penalties when marrying working fathers.

The takeaway is that H.R. 7024 would make most marriage penalties bigger (in the case of working single mothers), and make most marriage bonuses bigger (in the case of non-working single mothers). Most mothers work—including 76 percent of single mothers and 74 percent of married mothers—so the policy on net is likely to discourage marriage.

Overall, the per-child benefit provision of H.R. 7024 incentivizes part-time work (up to earnings of around $15,000 to $20,000), but discourages further progress either through full-time work or marriage. Policymakers concerned about marriage, upward mobility and self-sufficiency should carefully weigh these tradeoffs when considering H.R. 7024.