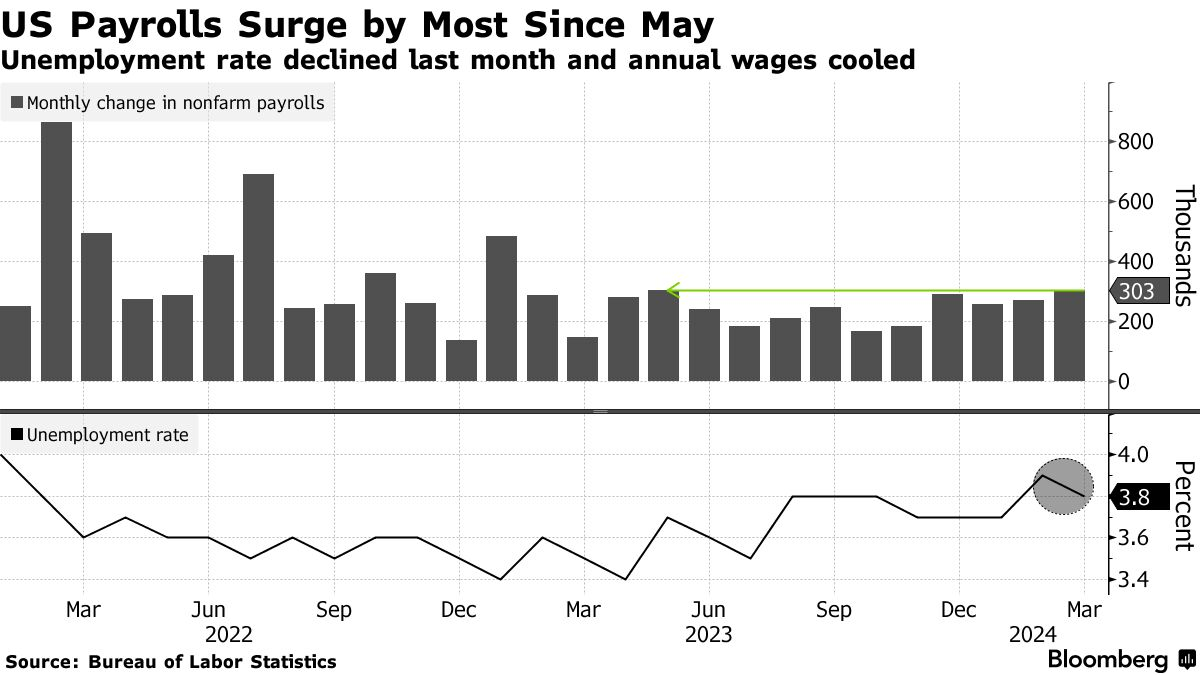

Economists were expecting 200,000 net new jobs added in March. Instead it was 50 percent more. Unexpected strength, but maybe not so unexpected, really, for an economy that continues to deliver surprise after surprise. It’s been a great run lately for economic optimists: real wage gains, faster labor productivity, and gobs of jobs.

A tight summary from RSM economist Joseph Brusuelas of what Americans are experiencing right now:

Employment data for some time now is consistent with what we refer to as a 3-2 condition — when unemployment rate stays in the 3% range, below 4%, and inflation is in the 2% range. Improved productivity, healthy immigration and an appropriate policy mix from the Federal Reserve can create the conditions for strong growth, price stability and maximum sustainable employment.

So, what’s not to like?

- In the short term, high inflation is still an issue. It remains stubbornly sticky, stirring fears of a possible resurgence, as was the pattern during the Great Inflation of the 1970s. Regarding the Federal Reserve’s inflation target of two percent, Chair Jerome Powell has acknowledged that traveling the final mile to that goal may be a bumpy ride. But he also suggests that the solid pace of economic growth gives policymakers flexibility to respond as new data come in. As Capital Economics argued in a morning note, “The blockbuster 303,000 increase in non-farm payrolls in March supports the Fed’s position that the resilience of the economy means it can take its time with rate cuts, which might now not begin until the second half of this year.”

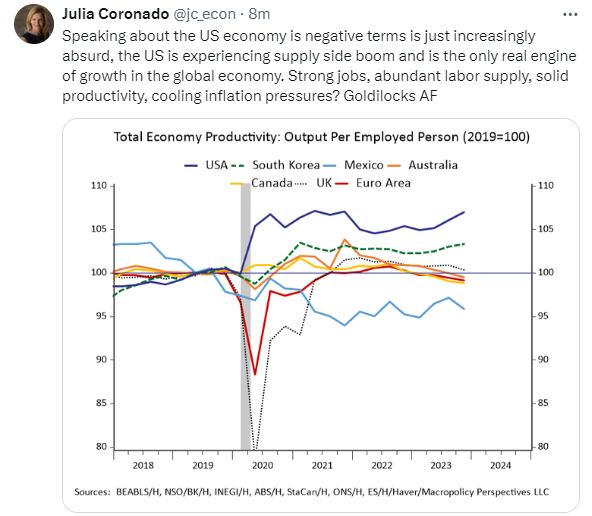

- Three consecutive quarters of strong productivity growth are great news, but it’s still too early to assume we are experiencing a sustained upturn. What we’re seeing right now might be more about post-pandemic normalization, such as the untangling of supply chains, rather than the impact of new technologies such as artificial intelligence. Washington should think hard about what policy can do to build upon recent gains, such as investing lots more in science research, permitting reform, and adopting a go-slow approach on AI regulation.

- Sorry to be a Debbie Downer about debt and deficits, but CBO predicts the national debt will nearly double to $48.3 trillion by 2034, and the debt-to-GDP ratio will reach 116 percent, up from 97 percent currently. Despite tax revenues exceeding the 50-year average, spending is projected to outpace historical levels, primarily driven by… wait for it… entitlement programs like Medicare, Social Security, and Medicaid. (Oh, and these forecasts may be optimistic since they assume no recession, expiration of tax cuts and subsidies, and no additional spending or debt cancellation efforts.) Growing deficits will compound interest payments, surpassing defense spending and reaching $1.6 trillion by 2034. If all this strikes you as unsustainable, you’re not wrong. A big productivity boom would be helpful here, but we shouldn’t count on it. The CBO doesn’t.

All that said, I would rather be in a position where I’m looking for weak spots in an expansion than sitting in a recession trying to find a silver lining.