The American Dream is celebrated as a core tenet of our society, promising opportunity and a better life through hard work and determination. Yet for many Americans, their pursuit of that dream has become harder, not for lack of effort but through the persistent rise of the cost of living.

A higher cost of living directly increases the difficulty of achieving a higher standard of living, requiring a higher income to afford the same bundle of goods and services. A higher cost of living also hinders opportunity, making neighborhoods with more employment opportunities, higher wages, better schools, and stronger communities effectively off-limits for lower-income families.

Federal policymakers can reduce the cost of living for all Americans through smart deregulation and by encouraging competition and innovation, enabling families to purchase more goods and services with a given income. Reducing federal debt can mitigate the risk of historically high levels of inflation returning. At the state and local levels, reducing overly burdensome restrictions on housing construction and childcare can increase access to high-opportunity neighborhoods.

The American Dream is too expensive. Its high price reduces Americans’ standard of living today and threatens the promise of a better life for future generations. Making the American Dream affordable requires urgent action from policymakers.

The Rising Cost of Living

When the prices of goods and services rise relative to household income, it becomes more difficult to afford a given standard of living. This is especially the case for items that make up a large share of household expenditures. As of 2023, the three items comprising the largest shares of consumer spending in the United States included housing (33 percent), transportation (17 percent), and food (13 percent).1 As reported in Figure 1, since 1980, the Consumer Price Index (CPI) for housing rose by 312 percent, the CPI for transportation rose by 226 percent, and the CPI for food rose by 281 percent. For comparison, nominal median household income grew by 355 percent over the 1980–2023 period. While incomes outpaced the price growth for these essential items, rising prices especially for housing have held back growth in real income.

The challenge of rising housing costs has been exacerbated in recent years by inflation-fueled high mortgage interest rates, combined with stubbornly high home prices resulting from limited housing supply. Similarly, food prices have risen quickly during the inflationary period starting in 2021. High inflation has eroded wage gains over the past several years.

Figure 1. CPI for All Urban Consumers and Nominal Median Household Income, 1980–2024

Source: US Department of Labor, Bureau of Labor Statistics, “Consumer Price Index for All Urban Consumers: Food in U.S. City Average,” Federal Reserve Bank of St. Louis, 2025, https://fred.stlouisfed.org/series/CPIUFDNS; US Department of Labor, Bureau of Labor Statistics, “Consumer Price Index for All Urban Consumers: Housing in U.S. City Average,” Federal Reserve Bank of St. Louis, 2025, https://fred.stlouisfed.org/series/CPIHOSNS; US Department of Labor, Bureau of Labor Statistics, “Consumer Price Index for All Urban Consumers: Transportation in U.S. City Average,” Federal Reserve Bank of St. Louis, 2025, https://fred.stlouisfed.org/series/CPITRNSL; and US Census Bureau, “Historical Income Tables: Households,” August 25, 2025, https://www.census.gov/data/tables/time-series/demo/income-poverty/historical-income-households.html.

Despite the growing cost of living, and particularly concerning price increases for certain items including housing, real living standards have nonetheless improved across the income distribution. This is especially the case when accounting for all sources of Americans’ income, including transfers, and adjusting for taxes. According to the Congressional Budget Office, since 1979, real posttax, post-transfer household income grew by 132 percent for Americans in the bottom quintile, 73 percent for the middle three quintiles, and 167 percent for the top quintile.2 While prices grew over time, after-tax income grew much faster. Income growth is due partly to an increase in labor force participation among women, which raises household income due to more market work. Still, average hourly earnings have grown since 1979 as well, just to a lesser extent than posttax, post-transfer household incomes, as Scott Winship recently documented.3

Americans have become materially better-off over time due to a growing economy. However, progress could be significantly faster if the cost of living, especially for major items like housing, had grown more slowly. Achieving the American Dream should be less expensive today than it is.

The Cost of Living and Opportunity

A higher cost of living makes it harder to achieve a better standard of living for all Americans. Just as importantly, particularly high living costs in certain geographic areas can restrict opportunity for Americans seeking a better life. In the past, it was common for Americans to move in pursuit of better employment, higher wages, and more opportunities for their children. Higher migration rates helped fuel convergence in areas’ economic fortunes over time: Free-flowing labor across geographic markets prevented persistently large wage gaps. However, this process began to break down starting in the 1980s. Migration rates have fallen. Distressed areas remain distressed. The result is less opportunity.

Economic opportunity encompasses the potential for financial security, economic advancement, access to high-quality education, and the availability of work and higher wages. Opportunity does not necessarily look the same for all people. A college-educated worker might view a dynamic city full of startups and innovative companies as a land of opportunity. Someone without a college degree might prioritize places with more jobs in manufacturing or the trades and the ability to move up through technical training without a requirement for advanced formal education. The problem is that if people cannot or do not move to opportunity, it can be much harder to access the American Dream, whatever it looks like for a particular individual, especially for those stuck in distressed areas that have little chance of improvement.

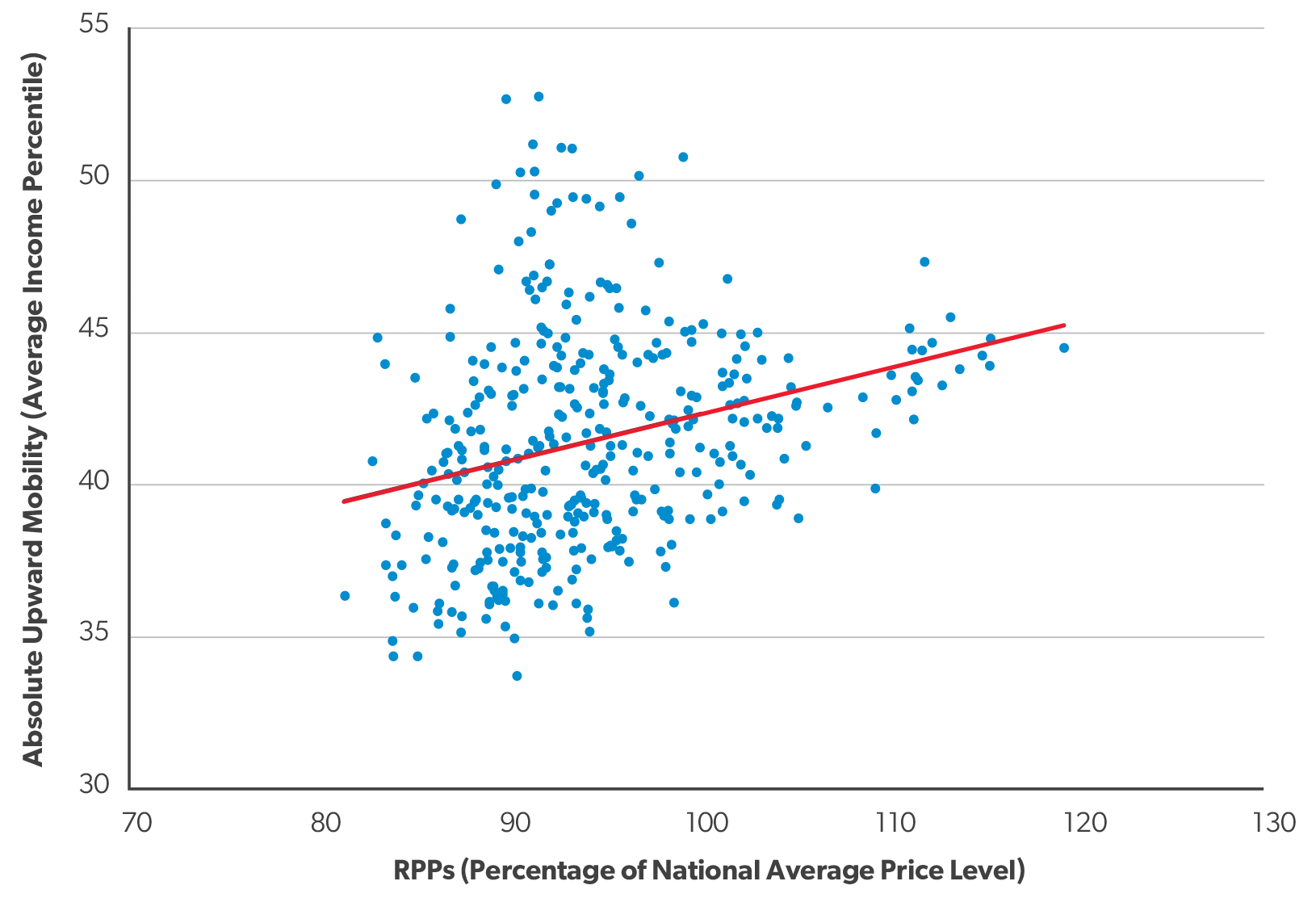

The biggest barrier to moving to opportunity is the high cost of living in areas with the most opportunity. Figure 2 illustrates the correlation between economic mobility and the cost of living. Here, economic mobility is defined as the income percentile of an adult who is raised in a household in the 25th income percentile. A higher value suggests that lower-income children are more likely to have a higher income when they become adults. The cost of living in an area is measured by its regional price parity (RPP), reflecting the price of all goods and services, though it is ultimately driven by housing-cost differences.4

In Figure 2, economic mobility and the cost of living have a positive relationship. This supports the hypothesis that high-cost areas could also have more opportunities, resulting in their higher average levels of economic mobility. This relationship could reflect ample high-paying job opportunities and advanced educational resources, which can significantly elevate the incomes of those who take advantage of these opportunities. This could result in high levels of economic mobility, with individuals seeing a real improvement in their financial status over that of their parents.

While higher-opportunity areas tend to have a higher cost of living, there are some exceptions to the rule. The highest levels of economic mobility were in 20 metro areas with a moderate cost of living. These include mostly smaller metropolitan areas with highly rated public school systems and affordable housing such as Dubuque, Iowa; Logan, Utah; and St. Cloud, Minnesota. This might suggest that there are regions in the US that are favorable to economic mobility and affordability.

The key for policymakers is to expand opportunity and promote affordability in as many places as possible. That means strengthening the mechanisms like good schools and strong communities that promote mobility while making areas with strong existing opportunities more affordable.

Where Is the Cost of Living High, and Why?

To bring down the cost of living, it is instructive to assess where the cost of living is the highest and why.

The cost of living varies significantly across states and cities. Hartville, Missouri (the geographic center of the US population that nearly 600 people call home), has a different cost of living than major cities like Washington, DC.5 Most of the difference in the cost of living between places is driven by the cost of housing (e.g., rent and home prices) and services (e.g., childcare). The cost of goods (e.g., clothes and groceries) also matters, but it is becoming less important as the prices of these products fall over the long run and geographic differences in markets become less important as more people shop online.6

Figure 2. Cost of Living and Upward Economic Mobility for Children

Source: Raj Chetty et al., “Where Is the Land of Opportunity? The Geography of Intergenerational Mobility in the United States,”

The Quarterly Journal of Economics 129, no. 4 (2014), https://doi.org/10.1093/qje/qju022; and US Department of Commerce, Bureau

of Economic Analysis.

Note: Every observation represents a metropolitan statistical area (blue dots). The red line represents the average absolute mobility rate for a given regional price level. The RPPs reflect the places where children are raised and are not necessarily where they end up as adults. The y-axis reflects the average income percentile in adulthood of children raised by parents at the 25th income percentile.

There is no single best measure of the differences in the cost of living between places. However, the US Bureau of Economic Analysis calculates RPPs to compare how prices for rents, services, and goods differ by state and metro area. These RPPs allow us to see how far a dollar goes. For example, the cost of living is about 31 percent higher in Washington, DC, than in Missouri. However, the cost of living is about 4 percent lower in Mississippi than in Missouri.7

Most of the difference in the cost of living in Washington, DC, is driven by higher housing costs. For example, in Hartville, the median cost of a home is about $300 per square foot, while in DC the median cost is about $530.8 The median monthly rent of a three-bedroom apartment in Hartville is $1,155, compared with $3,112 in DC.9 These differences affect not only housing affordability but also residents’ overall lifestyle and savings potential. However, most of the difference in the cost of living in Mississippi relative to Missouri is driven by lower costs for services, as housing costs are quite low (comparatively) in Missouri.10

High home prices and rents are the result of a constrained housing supply in the face of strong demand. When a sufficient number of homes cannot be built to meet demand, prices are forced to rise. Supply is foremost constrained by onerous state and local restrictions on building housing, such as undue environmental reviews, minimum lot sizes, parking requirements, and red tape that delays and slows construction.

Escalating childcare costs also burden household finances and increase the overall cost of living for families with young children.11 Childcare centers face rising operational costs, including hiring staff, maintaining up-to-date facilities, and adhering to increasingly stringent regulatory standards. Meanwhile, high childcare costs can deter parents from returning to the workforce, thereby affecting labor market participation rates and economic productivity.12 Additionally, when a substantial portion of a family’s income is allocated to childcare, less is available for other expenditures, which can reduce overall economic activity and demand within the economy.

In many cities, strong demand for childcare in tandem with limited supply pushes up prices.13 The problem is worse in densely populated cities, where space is at a premium, driving up rental costs for facilities. Moreover, as more families become dual-income households, the need for reliable childcare grows, further increasing demand and prices.

As more people become aware of the importance of early childhood development, expectations for high-quality childcare rise. Parents increasingly seek centers that offer not only basic care but also educational programming and developmental activities. Meeting these expectations involves additional costs, from hiring specialized staff to investing in educational materials and activities, which in turn further elevates the cost of childcare services.

The childcare industry faces significant staffing challenges. Despite the nature of their work, childcare providers often receive low wages, leading to high turnover and a persistent shortage of qualified professionals. Some cities, including Washington, DC, have instituted higher educational requirements for day care providers. As of December 2023, all city day care providers must hold at least an associate degree.14

However, essential skills for childcare, such as patience, empathy, and the ability to engage young children, are not necessarily acquired through formal education. These requirements may elevate the perceived quality of care but do not directly correlate with the actual needs and dynamics of early childhood care. Furthermore, they exclude many qualified applicants from the workplace, limiting the supply of workers and raising costs.

In response to the high and rising cost of living, especially for housing and childcare, many residents in high-cost urban areas have been moving to suburban or rural areas, where costs are generally lower. This trend might become even more amplified by the increased flexibility of remote-work options due to the COVID-19 pandemic. With the ability to work from anywhere, many have opted to leave more expensive cities for places where they can get more space and a better quality of life for their money.15

Apart from suburban and rural shifts, there is also a noticeable trend of people moving from high-cost states such as California and New York to lower-cost states such as Arizona, Florida, and Texas. These states not only offer more affordable housing but also tend to have lower taxes, which can be a significant draw.16 A 2020 report from the George W. Bush Institute at Southern Methodist University found that metropolitan areas that drew people all shared the same characteristics: They had good job markets with high-productivity industries, an affordable housing supply that was growing, low levels of economic segregation, favorable regulatory environments for starting new businesses, and high levels of social capital.17

The lesson for high-cost areas is that to ensure strong economic growth, they must act to relieve their high-cost burdens. That will not only allow their cities to prosper economically but also provide more families access to opportunity at a price they can afford.

The Price of Debt and the Cost of Living

The high cost of living that American families face is driven by not only local policies but national ones as well, including through those policies’ role in determining the price of borrowing. The price of borrowing money is the interest we pay on debt. Rising interest rates can significantly affect the cost of living for individuals and families because their effect on everyday expenses is widespread, from housing costs to consumer spending. Interest rates also affect consumer sentiment, which can affect the economy.18

One of the most direct effects of higher borrowing costs is on housing. Homeowners with variable-rate or adjustable-rate mortgages experience immediate increases in their monthly payments when interest rates rise. This increase in mortgage costs can consume a larger portion of household income, reducing the amount available for other expenses and savings, thus elevating the overall cost of living. For those looking to buy homes, higher rates mean more expensive mortgage financing, potentially putting homeownership out of reach.

The effect on renters is similarly burdensome. Landlords could increase rent to cover the heightened costs of their mortgage payments, translating into higher living expenses for tenants. This adjustment can particularly affect those in cities with already pricey rental markets, exacerbating affordability issues and possibly leading to a higher rate of tenant turnover or difficulties in finding affordable housing.

Higher interest rates also affect all forms of consumer credit. Credit card rates, closely tied to the Federal Reserve’s actions, increase with policy adjustments. This rise means that consumers with credit card balances will see their interest expenses climb, reducing their effective disposable income. Similarly, auto loans and personal loans also become more expensive. The increased cost of servicing these debts can deter new consumer spending and constrain financial flexibility, further increasing the cost of living by limiting how much consumers can spend on necessities and discretionary items.

The broader economic implications of higher borrowing costs include a slowdown in business investment. Businesses may delay or scale back plans for expansion or new investments as borrowing becomes more expensive. That, in turn, can lead to slower economic growth, affecting employment levels and wage growth. A sluggish economy often means fewer job opportunities and smaller wage increases, which are critical in maintaining or improving living standards. When businesses face higher costs of capital, these expenses can be passed on to consumers in the form of higher prices for goods and services, adding to the inflationary pressures that central banks aim to control by raising rates.

Governments are not immune to higher interest rates either. Increasing the cost of borrowing can lead to higher public-debt servicing costs, which might necessitate increases in taxes or cuts in public spending. Increased taxes reduce disposable income, whereas reduced public spending can mean less access to public services such as education, health care, and infrastructure maintenance. These changes can elevate the overall cost of living, making daily life more expensive and potentially less secure.

While the Federal Reserve’s primary reason for raising interest rates is often to combat inflation, the effect on the cost of living is complex. In the short term, the increased costs of borrowing can lead to higher prices as businesses pass on higher costs to consumers, which diminishes consumers’ purchasing power. If the rate increases successfully temper inflation over time by reducing demand for borrowing, prices could stabilize. However, the transition period can be marked by price volatility, which complicates household budgeting. The best solution is to avoid high inflation in the first place.

Expanding Opportunity by Lowering the Cost of Living

In addressing the cost of living, policymakers often resort to measures such as price controls and subsidizing demand. These interventions tend to be politically popular because they appear to provide immediate relief.19 However, while well-intentioned, such policies can have unintended consequences that could exacerbate the very problems they are trying to solve.

Price controls, for instance, can discourage producers from increasing supply or investing in production due to reduced profitability. When the supply of a product is relatively fixed, demand subsidies can lead to an increase in price without increasing the product’s quantity or quality. Producers could then raise prices, therefore capturing the subsidy. Thus, these measures, though initially appealing for their direct impact, can inadvertently lead to increased costs over the long term.

There is a long history demonstrating that price controls do not work as intended.20 For example, research by Rebecca Diamond and colleagues found that rent control policies ultimately increased market rents by weakening landlords’ incentive to rent out apartments.21 There are also many examples of demand subsidies failing to reduce the cost of living. In housing, demand subsidies encourage “more dollars [to] chase the same number of homes.”22 This is because potential buyers bid up home prices when supply constraints limit the building of additional homes. Another recent example is the federal government subsidizing the demand for broadband, which does not significantly change the number of people who can afford high-speed internet but does increase prices by eliminating low-cost plans.23

A better, more sustainable policy would be to focus on deregulation and increasing competition. In essence, governments at all levels should allow market efficiencies and private-sector innovation to drive down costs.

One recent case of how deregulation reduced prices was in 2017, when Congress nullified a rule enacted by the Federal Communications Commission (FCC) regarding consumer data sharing. Before the FCC’s rule was enacted, internet service providers could share consumer data with companies unless the consumer opted out of the data-sharing arrangement. Companies designed plans that allowed consumers to opt in or out of data sharing at different subscription rates. In essence, those who opted in paid lower rates than those who opted out because companies would sell those consumer data and use them to reduce the price of the internet service.

The FCC enacted a rule in 2016 that required consumers to opt in to a data-sharing model. However, Congress used the Congressional Review Act process to cancel this rule in 2017. The 2020 Economic Report of the President found that overturning the FCC’s rule requiring consumers to opt in to data sharing had reduced wireless prices by more than 10 percent and wired prices by as much as 2 percent.24

The same effects of deregulation occurred in health care when the Food and Drug Administration approved more generic drugs, which the Trump administration spurred with its Promoting Healthcare Choice and Competition Across the United States executive order.25 This increase in available generic drugs led to an 11 percent reduction in prescription drug prices.26 The Trump administration also permitted more small businesses to form association health plans and allowed short-term limited duration plans, which together reduced health insurance premiums and increased real incomes.27

Moving forward, policymakers should heed the lessons of past failures and successes to reduce the cost of living. That requires pursuing deregulation, promoting tax reform, encouraging competition and innovation, and reducing the federal deficit.

Deregulation Should Be Central to Reducing the Cost of Living

Deregulation involves removing unnecessary regulatory barriers that are not grounded in safety and can stifle competition and raise costs. One of the areas ripest for deregulation is housing and real estate development. Zoning laws, for example, restrict the supply of new housing, driving up prices. By relaxing these laws, governments can encourage the development of more housing units, which can help stabilize or reduce prices by increasing supply.

Eliminating unnecessary building codes and regulations can significantly increase the housing supply by streamlining the construction process and reducing development costs.28 Such deregulation makes it easier and more cost-effective for builders to bring new homes to market, which can alleviate housing shortages and drive down prices. By removing these bureaucratic hurdles, policymakers can foster a more dynamic and responsive housing market that better meets residents’ needs.

A recent success story is Austin. In the wake of the COVID-19 pandemic, Austin was facing growing housing demand with the rise of remote work and more people seeking to move to the city. Austin relaxed restrictions on minimum lot sizes, enabled multiple units to be constructed on single-family plots, and approved more apartment buildings. The result? Rents are now falling in Austin.

While the onus is largely on states and localities to cut regulations that constrain housing supply, the federal government should not stand in the way or think that by simply stimulating demand it can address the housing affordability crisis.

Childcare can also benefit from scaling back the overregulation that has increased costs for families. Easing the stringent educational requirements for day care providers can help address the shortage of available childcare options and reduce costs for families. By allowing individuals with practical experience and appropriate certifications to enter the field, we can expand the workforce and increase access to quality childcare without the burden of excessive prerequisites that might not directly correlate with better care.

Sometimes, an effective approach to deregulation can also be implementing a smarter, more efficient regulatory process. For example, getting the right permits can often take a long time and involve uncertainty. This is a problem at the federal, state, and local levels. However, some governments are experimenting with new processes. Virginia launched a new transparency program in 2022 for permits that the Department of Environmental Quality processes to address the costs associated with slow permitting.29 This program intends to speed up the time it takes for the permits to move through the process and through public accountability.30

Another idea to speed up the regulatory process is to auction fast-track permitting to the private sector. Under this proposal, individuals or businesses applying for permits could bid on a fixed number of slots for the fast-track authority that would guarantee them a decision on the permit in a reasonable period. They would pay for the fast-track authority only if they ultimately received the permit.

Tax Reform Can Help

Local governments use property taxes to fund essential services such as schools, roads, and emergency services. However, these taxes also affect the cost of living for the community’s residents and businesses.

For homeowners, property taxes add to the cost of owning a home. Although renters do not directly pay property taxes, they indirectly feel the effects through higher rent. Landlords often pass these costs on to tenants to maintain profitability on their properties. Businesses, especially those that own property, also bear the burden of property taxes. Like landlords, business owners typically pass on the costs to consumers through higher prices for goods and services.

High property taxes can also be a barrier to homeownership, particularly for lower-income households. Homeownership is often a critical means for building wealth over time. Local and state governments should look to better tax systems that tax what people buy rather than what people own in the form of property to encourage economic mobility.

The federal government could also implement changes in the tax code to enhance housing affordability. For instance, under the current tax system, taxpayers are allowed a mortgage interest deduction on non-primary residences. By eliminating or significantly reducing this benefit, Congress could produce multiple positive outcomes, including an increase in the availability of homes for primary-residence buyers. This reform not only would adjust the housing market to favor occupancy rather than investment but could stabilize housing prices and improve overall accessibility.

More generally, income tax deductions often subsidize purchases that would have been made without the deduction. These tax breaks increase the cost of these purchases (because sellers can capture some of the benefit by raising prices), which makes them less affordable for lower-income families, who cannot hope to benefit from the deduction. Examples include the state and local tax deduction’s impact on housing costs and the impact of tax breaks for childcare on costs in that sector.

Encourage Competition and Innovation

Competition and innovation are central to any policy agenda to lower the cost of goods and services. When businesses compete, they are incentivized to innovate, improve quality, and reduce prices to attract customers. Furthermore, governments at all levels can smother innovation through overregulation, which can increase the cost of living both within and beyond their borders.

One area where there are considerable possibilities for increased innovation is in the adoption of artificial intelligence. For example, AI can analyze vast amounts of data to identify patterns and efficiencies that humans could overlook, optimizing everything from supply-chain logistics to energy use, thereby reducing production costs and, consequently, consumer prices. Additionally, AI-driven automation can perform repetitive tasks more efficiently than human workers, potentially lowering costs in industries ranging from manufacturing to customer service.

Furthermore, AI can help create new products and services that can provide more free time or reduce the cost of basic household goods. For instance, in financial services, AI can help individuals optimize their savings and spending, while in health care it can predict patient health trends and tailor treatments to improve outcomes and reduce costs.

However, overregulation can get in the way. In 2023, President Joe Biden signed an executive order creating a new regulatory framework that goes well beyond making sure that AI is safe.31 Government agencies, such as the National Institute of Standards and Technology and the National Telecommunications and Information Administration at the US Department of Commerce, have hired regulators that could apply a heavy hand to the burgeoning industry, including the promotion of “algorithmic justice.”32 Meanwhile, many states are introducing new regulatory approaches that could limit competition by favoring existing market participants or restricting the possibility of AI’s advances.33

Other strategies for increasing competition and innovation include investing in research and development and patent reforms.

Reducing the Federal Deficit Will Reduce Inflation and Prices

Fiscal discipline can have indirect but profound effects on the cost of living. By avoiding excessive borrowing and large fiscal deficits, governments can help keep interest rates low, which encourages investment and curbs inflation. This fiscal discretion ensures that future generations are not burdened with high taxes to pay off today’s debt, thereby stabilizing long-term economic conditions and keeping the cost of living manageable. This is especially important today, as so much of the federal government’s spending is paid for with new debt and money creation.34

Conclusion

These strategies demonstrate how reducing government intervention can effectively decrease the cost of living. Other sector-specific strategies in, for instance, health care and higher education can similarly increase affordability while expanding opportunity. By fostering an environment in which market forces and private-sector efficiencies exist alongside necessary protections, governments can help maximize economic benefits. This balanced approach can lead to sustainable economic growth and an improved standard of living for all Americans.

Notes

- US Department of Labor, Bureau of Labor Statistics, “Consumer Expenditures—2023,” press release, September 25, 2024, https://www.bls.gov/news.release/archives/cesan_09252024.pdf.

- Ellen Steele and Bilal Habib, Trends in the Distribution of Household Income from 1979 to 2021 , Congressional Budget Office, September 11, 2024, https://www.cbo.gov/publication/60342.

- Scott Winship, Understanding Trends in Worker Pay over the Past 50 Years, American Enterprise Institute, May 14, https://www.aei.org/research-products/report/understanding-trends-in-worker-pay-over-the-past-50-years/.

- US Department of Commerce, Bureau of Economic Analysis, “Real Personal Consumption Expenditures by State and Real Personal Income by State and Metropolitan Area, 2023,” press release, December 12, 2024, https://www.bea.gov/news/2024/real-personal-consumption-expenditures-state-and-real-personal-income-state-and.

- US Census Bureau, “2020 Census Center of Population Data Visualization,” November 16, 2021, https://www.census.gov/library/visualizations/interactive/2020-census-center-of-population.html.

- Author’s calculations using RPP data from the US Bureau of Economic Analysis.

- Author’s calculations using RPP data from the US Bureau of Economic Analysis.

- Realtor.com, website, accessed April 2024, https://www.realtor.com/.

- US Department of Housing and Urban Development, Office of Policy Development and Research, “50th Percentile Rent Estimates,” 2025, https://www.huduser.gov/portal/datasets/50per.html.

- Author’s calculations using RPP data from the US Bureau of Economic Analysis.

- White House, “The Cost of Living in America: Helping Families Move Ahead,” August 11, 2021, https://web.archive.org/web/20240702112528/https://www.whitehouse.gov/cea/written-materials/2021/08/11/the-cost-of-living-in-america-helping-families-move-ahead/.

- Taryn W. Morrissey, “Child Care and Parent Labor Force Participation: A Review of the Research Literature,” Review of Eco nomics of the Household 15, no. 1 (2017): 1–24, https://link.springer.com/article/10.1007/s11150-016-9331-3.

- US Department of the Treasury, The Economics of Child Care Supply in the United States , September 2021, https://home.treasury.gov/system/files/136/The-Economics-of-Childcare-Supply-09-14-final.pdf.

- Tara Bahrampour, “D.C. Child-Care Workers Celebrate Their New Degrees,” The Washington Post , March 30, 2023, https://www.washingtonpost.com/dc-md-va/2023/03/25/childcare-worker-dc-degree-mandate/.

- The relationship between remote work and cost of living is not straightforward because not all jobs can be transitioned to remote work. That said, Lukas Althoff et al. find that many business services that were concentrated in expensive, large cities could transition to remote work, and this is where the largest such transitions have been. For example, more than half of business services were shifted to remote work during the first months of the COVID-19 pandemic. Lukas Althoff et al., “The Geography of Remote Work,” Working Paper No. 29181 (National Bureau of Economic Research, August 2021), https://www.nber.org/system/files/working_papers/w29181/w29181.pdf.

- J. H. Cullum Clark, “Americans Keep Moving to High-Opportunity Cities in the Sun Belt, New Census Data Confirms,” George W. Bush Presidential Center, April 7, 2023, https://www.bushcenter.org/publications/america-keeps-moving-to-high-opportunitycities-in-the-sun-belt-new-census-data-confirms; and J. H. Cullum Clark, Cities and Opportunity in 21st Century America, George W. Bush Institute–SMU Economic Growth Initiative, November 2020, https://gwbushcenter.imgix.net/wp-content/uploads/gwbi_2021_CitiesOpportunity.pdf.

- Clark, Cities and Opportunity in 21st Century America.

- Marin A. Bolhuis et al., “The Cost of Money Is Part of the Cost of Living: New Evidence on the Consumer Sentiment Anomaly,” Working Paper No. 32163 (National Bureau of Economic Research, February 2024), https://www.nber.org/papers/w32163.

- Christopher S. Elmendorf et al., “What State Housing Policies Do Voters Want? Evidence from a Platform-Choice Experi ment” (working paper, Social Science Research Network, November 17, 2025), https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4811534.

- Eamonn Butler, “Price Controls Have Been Disastrous Throughout History,” in War on Prices: How Popular Misconceptions About Inflation, Prices, and Value Create Bad Policy, ed. Ryan Bourne (Cato Institute, 2024).

- Rebecca Diamond et al., “The Effects of Rent Control Expansion on Tenants, Landlords, and Inequality: Evidence from San Francisco,” The American Economic Review 109, no. 9 (2019): 3365–94, https://www.aeaweb.org/articles?id=10.1257/aer.20181289.

- M. Nolan Gray, “Help Homebuyers by Expanding Supply,” City Journal, June 7, 2021, https://www.city-journal.org/article/help-homebuyers-by-expanding-supply.

- Paul Winfree, Bidenomics Goes Online: Increasing the Costs of High-Speed Internet , Economic Policy Innovation Center, January 8, 2024, https://epicforamerica.org/publications/bidenomics-goes-online-increasing-the-costs-of-high-speed-internet/; and Paul Winfree, “Testimony by Paul Winfree, Ph.D.,” testimony before the Senate Committee on Commerce, Science, and Transportation, Subcommittee on Communications, Media, and Broadband, May 2, 2024, https://www.commerce.senate.gov/services/files/AD27868D-118B-4547-B8E4-32F100BC7D62.

- White House, Economic Report of the President: Together with the Annual Report of the Council of Economic Advisers , February 2020, https://web.archive.org/web/20220427193221/https://www.whitehouse.gov/wp-content/uploads/2021/07/2020-ERP.pdf.

- Exec. Order No. 13813, 82 Fed. Reg. 48385 (2017).

- White House, Economic Report of the President.

- White House, Economic Report of the President.

- Howard Husock, “We Don’t Need Subsidized Housing,” City Journal, Winter 1997, https://www.city-journal.org/article/we-dont-need-subsidized-housing.

- Virginia Permit Transparency, “About VPT,” https://permits.virginia.gov/Home/About.

- James Broughel, Transparency on Tap: Virginia’s Online Permit Revolution, Competitive Enterprise Institute, June 2024, https://cei.org/wp-content/uploads/2024/06/Fast_Track_-_Transparency_on_Tap_-_Virginias_online_permit_revolution_0424_4.pdf.

- Exec. Order No. 14110, 88 Fed. Reg. 75191 (2023).

- Paul Winfree, “Hidden Funding: ‘Algorithmic Justice’ for Artificial Intelligence,” Economic Policy Innovation Center, March 4, 2024, https://epicforamerica.org/blog/hidden-funding-algorithmic-justice-for-artificial-intelligence/.

- Adam Thierer, “California and Other States Threaten to Derail the AI Revolution,” R Street Institute, May 2, 2024, https://www.rstreet.org/commentary/california-and-other-states-threaten-to-derail-the-ai-revolution/.

- Paul Winfree, “New Debt Has Paid for 76% of Federal Spending Since 2020,” Economic Policy Innovation Center, September 26, 2024, https://epicforamerica.org/blog/new-debt-has-paid-for-76-of-federal-spending-since-2020/.